Financial accounting requires that financial statements be issued following the end of an accounting period. Managerial accounting may issue reports much more frequently, since the information it provides is of most relevance if managers can see it right away. Financial accounting reports on the profitability (and therefore invoice management guide for beginners and pros alike the efficiency) of a business, whereas managerial accounting reports on specifically what is causing problems and how to fix them. Managerial accounting reports are more likely to be of use in improving operations, while financial accounting reports are used by outsiders to decide whether to invest in or lend to a business.

- In accounting, a conservatism principle is often applied, which suggests that companies should record lower projected values of their assets and higher estimates of their liabilities.

- After the accruals (which affect both the COGS and OPEX accounts), she prepares Primark’s Income Statement for a final review.

- Also, since no external standards are imposed on information provided to internal users, management accounting reports run the risk of being subjective.

- A cash flow statement tracks the actual cash flowing in and out of a company in a given accounting year.

Adhering to Compliance Requirements

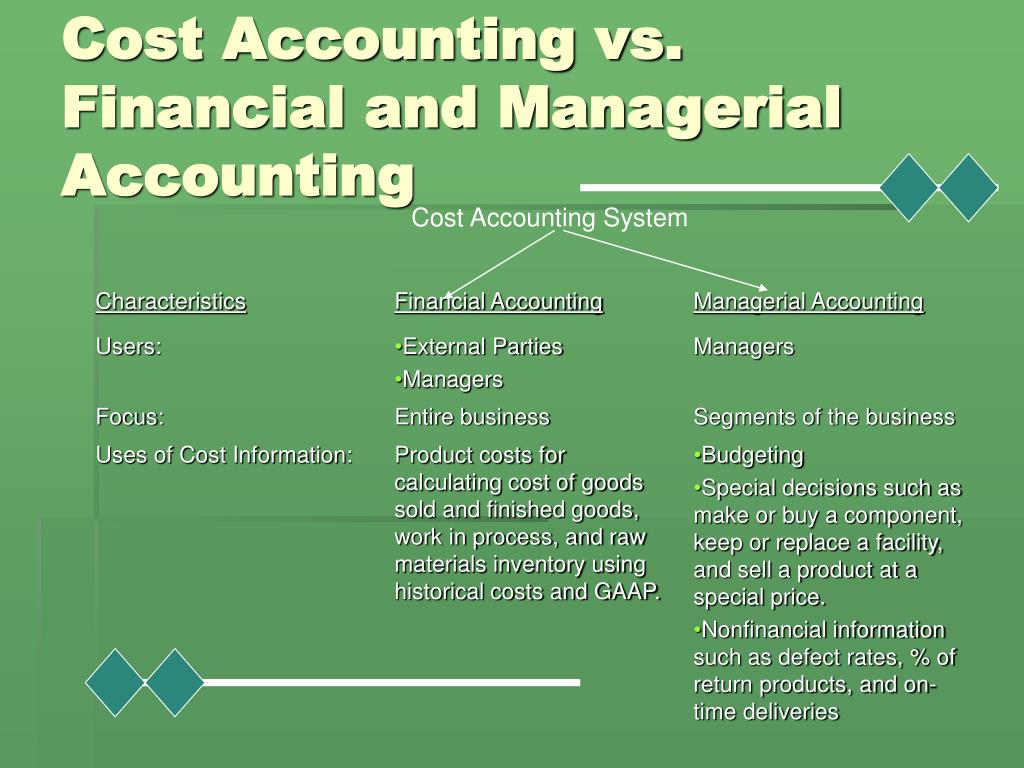

Accounting is crucial in ensuring that a company fulfills its goals and updates strategies to its needs. It includes the standards, conventions and rules that accountants follow in recording and summarizing and in the preparation of financial statements. In the managerial accounting vs. financial accounting decision facing students, one major distinction is the audience for the financial reports each position prepares. The key difference between managerial accounting and financial accounting relates to the intended users of the information.

Difference Between Financial and Management Accounting

The specialized needs of specific users are satisfied through supplementary reports, which are published at various intervals (e.g., annually or quarterly). Managerial accounting statements can be drawn up by Certified Management Accountants (CMAs), while financial accounts are drawn up by Certified Public Accountants (CPAs). We also allow you to split your payment across 2 separate credit card transactions or send a payment link email to another person on your behalf.

Reporting Focus

By dividing the business into smaller sections, a company is able to get into the details and analyze the smallest segments of the business. Financial accounting provides information to enable stockholders, creditors, and other stakeholders to make informed decisions. This information can be used to evaluate and make decisions for an individual company or to compare two or more companies. However, the information provided by financial accounting is primarily historical and therefore is not sufficient and is often synthesized too late to be overly useful to management.

Financial Accounting

Moreover, financial statements are released on a regular schedule, establishing consistency of external information flows. Managerial accounting involves identifying, measuring, analyzing, interpreting, and communicating financial information to an organization’s managers for pursuit of that organization’s goals. Unlike accounting’s reliance on transactional data, finance looks at how effectively an organization generates and uses cash through the use of several measurements. The field of finance can be broken down to hone in on the specific types of parties involved, including personal finance, corporate finance, and public finance. While these categories typically include a similar set of activities, each type of finance has nuances that reflect the different regulations, considerations, and concerns of each population. Because it is manager oriented, any study of managerial accounting must be preceded by some understanding of what managers do, the information managers need, and the general business environment.

While the focus of managerial accounting is internal, the focus of financial accounting is external, with a focus on creating accurate financial statements that can be shared outside the company. Managerial accounting typically runs a variety of operational reports throughout the month, while financial accounting runs financial statements at the end of the accounting period. Financial accounting follows generally accepted accounting principles (GAAP), which are a set of accounting standards that are recognized by the accounting profession and regulators.

Companies are often looking for ways to gain a competitive advantage, so they examine a lot of information that might be hard to understand for outside parties. Their deep understanding of company transactions allows them to specialize in financial reporting or managerial reporting. Managerial accounting reports are highly detailed, technical, specific, and even exploratory in nature. Companies are always looking for a competitive advantage, so they may examine a multitude of details that could seem pedantic or confusing to outside parties.

These details are used to prepare financial statements summarizing the financial transactions of a given accounting period. Both financial accounting and managerial accounting provide valuable information for analyzing the performance and profitability of a business. Budgeting, forecasting, and planning are key areas where financial accounting and managerial accounting intersect. Both types of accounting rely on these processes to make informed decisions and manage financial resources effectively.

One key difference between the two is the level of detail provided in operational reports. Managerial accounting provides detailed operational reports that allow managers to analyze the efficiency of different departments and processes within the company. This information can be used to improve profitability by identifying areas where costs can be reduced and revenue can be increased.